Silence is Not Consent: SunEdison Court Rejects Third Party Releases by Passive Consent

In today’s chapter 11 practice, third party releases are ubiquitous. A staple of the largest and most complex cases for years, plan provisions releasing and enjoining claims against non-debtors, particularly officers and directors, are now common place in most business reorganizations. While case law permits a bankruptcy court to enjoin claims against non-debtors in limited, fact-specific circumstances, plan proponents frequently achieve far broader releases by creditor consent. In re SunEdison, Inc. [1] presents a cautionary tale of a company and its major creditors who audaciously pushed the boundaries of creditor consent and, in so doing, may have overreached.

Consensual releases of non-debtors (i.e., “third party releases”) come in all shapes and sizes: creditors consent to the proposed release by voting for the plan or against the plan; by “opting in” or “opting out” of the release on their ballot; and sometimes creditors whose votes are solicited by the debtor are deemed to have consented to the release by failing to take any action whatsoever. Ordinarily, the debtor negotiates the contours of third party releases with lenders and committees of creditors and bondholders prior to the disclosure statement hearing. Bankruptcy courts tend to focus on adequate disclosure and sufficient notice of the release in the plan solicitation materials, and third party releases are often approved upon plan confirmation without further discussion.

In a decision that is likely to reshape the debate, at least in one popular venue, a Bankruptcy Judge for the Southern District of New York has challenged conventional thinking about third party releases in bankruptcy by asking whether a creditor can be deemed to have released non-debtor third parties simply by failing to vote on a chapter 11 plan. SunEdison suggests that the tide may be turning on consensual third party releases.

1. SunEdison Bankruptcy

SunEdison, Inc. (“SunEdison”) was once the largest renewable-energy development company in the world. At its peak, SunEdison did it all: It built renewable energy plants, financed renewable energy plants, owned plants, operated plants, and even managed renewable energy plants for third parties. The energy giant grew rapidly, borrowing heavily to finance new projects ($24 billion in three years) for its massive “yieldcos.” [2] The debt burden eventually became unsustainable and, as its stock price dipped, investor confidence waned, resulting in “the Biggest Corporate Implosion in US Solar History.” [3]

On April 21, 2016, SunEdison and 50 affiliates (the “Debtors”) filed for relief under chapter 11 of the Bankruptcy Code [4] in the United States Bankruptcy Court for the Southern District of New York (the “Bankruptcy Court”). SunEdison was a complex case in every sense, with hundreds of millions of dollars in debtor-in-possession (“DIP”) financing, dozens of retained professionals, bespoke sale and claims resolution procedures, and over 6,200 proofs of claim filed. SunEdison’s organizational structure consisted of approximately two thousand distinct corporate entities, many which remained outside of bankruptcy (the “Non-Debtors”) even though the energy projects owned by the Non-Debtors were supported by DIP funding and sold by the Debtors pursuant to special procedures that did not require the traditional notice and hearing.

As is typical of most reorganizations as sprawling and complex as SunEdison’s, the companies’ First Amended Joint Plan of Reorganization (the “Plan”) included an extremely broad third-party release (the “Release”), which would enjoin actions against a wide array of non-debtor parties. On July 28, 2017, Judge Stuart M. Bernstein confirmed the Plan but reserved decision on whether the Release could be approved. A month later, in a decision issued on November 8, 2017, Judge Bernstein declined to approve the Release as proposed. [5]

2. The Third Party Release

Section 11.6 of the Plan, entitled “Release by Holders of Claims,” provided a broad release of all claims relating to the Debtors and the transactions undertaken in the bankruptcy, with a standard carve-out for claims arising through fraud, willful misconduct, and gross negligence. [6] The Release protected and ran in favor of the “Released Parties”: an extensive cast of characters that included the Debtors, the Non-Debtors, the Debtors’ pre- and post-petition lenders, the Creditors’ Committee, officers, directors, employees, and professional advisors of all stripes. [7] The list of “Releasing Parties” was equally long and included “to the fullest extent permitted by law, all Holders of Claims entitled to vote for or against the Plan that do not vote to reject the Plan.” [8] In other words, the Release applied not only to creditors who affirmatively voted in favor of the Plan, but also to those who did not vote or return a ballot (the latter, the “Non-Voting Creditors”). The Release was coupled with an injunction provision that barred the pursuit of any released claim. [9]

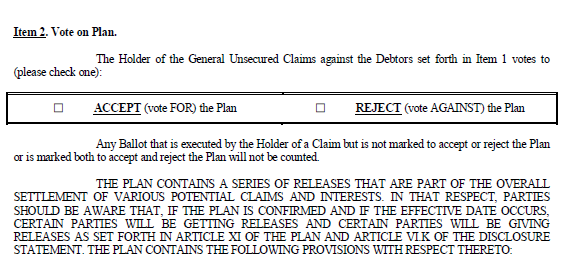

The SunEdison Plan ballots, in relevant part, looked like this:

Rather than separate a creditor’s vote from its release of the Released Parties (via an “opt in” or “opt out” box), a creditor’s consent to the Release was inseparable from the mechanics of voting. To understand the consequences of failing to vote, Non-Voting Creditors had to read through a complex definition of Releasing Parties and deduce that only by voting to reject the Plan would they preserve any claims against the Released Parties.

When confirmation of the Plan was put before the Bankruptcy Court, no party in interest questioned whether the Release was permissible. Nevertheless, Judge Bernstein raised the issue, sua sponte. [10] In his decision, Judge Bernstein first examined whether, by failing to vote on the Plan, Non-Voting Creditors had implicitly consented to the Release. He then considered the circumstances under which a bankruptcy court has the authority to approve a third party release irrespective of creditor consent.

3. Release by Implied Consent

Canvassing applicable case law on the subject, Judge Bernstein acknowledged that several bankruptcy courts have held that chapter 11 plans may include third party releases that are predicated upon consent by the affected creditors. [11] In 2008, Bankruptcy Judge Robert Gerber held in In re DBSD North America, Inc., that third party release provisions were permissible on the basis of consent. In DBSD, the debtors’ plan provided that creditors who voted in favor of the plan, or abstained from voting and failed to “opt out” of the exculpation provisions, were deemed to have consented to the third party release. [12] Significantly, Judge Gerber found that the release provisions were conspicuously set off in bold font in the disclosure statement and ballots, thereby providing adequate notice to creditors of the consequences of failing to opt out. Judge Brendan Shannon of the United States Bankruptcy Court for the District of Delaware approved a similar release in In re Indianapolis Downs, LLC. [13] Judge Shannon found that the debtors’ solicitation package provided creditors with detailed instructions on how to opt out from the plan release provisions.

In their respective decisions in DBSD and Indianapolis Downs, Judges Gerber and Shannon focused on the adequacy of the notice provided to creditors. Both courts assumed that creditor consent to a third party release could be implied if the creditor failed to do something that was clearly and conspicuously set out in the solicitation materials. [14]

Judge Bernstein took an entirely different approach in SunEdison. While Judge Bernstein agreed that an affirmative vote to accept the Plan would constitute express consent to the Release, he found that “deemed consent” by failing to return a ballot presented a closer question. He viewed implied consent, first and foremost, as contractual issue to be decided under applicable state law. [15] Judge Bernstein noted a generally accepted principle of contract law that, absent a duty to speak, silence does not constitute consent. [16] New York law, which Judge Bernstein applied, recognizes three exceptions to this rule. Assent by silence may be inferred where: (1) it is supported by the parties’ ongoing course of conduct; (2) the offeree (i.e., the releasing party) accepts the benefits of the offer despite a reasonable opportunity to reject them; or (3) the offeror has given the offeree reason to understand that silence will constitute acceptance and the offeree in remaining silent intends to accept the offer. [17]

Judge Bernstein was not persuaded that the Releasing Parties’ silence should be deemed their consent to the Release. [18] Specifically, the Debtors could not identify to Judge Bernstein’s satisfaction the source of the creditors’ duty to speak on the Release. The Debtors argued that the language in the disclosure statement and plan ballots describing the Release provided sufficient warning of the potential effect of silence, thereby creating such duty. [19] Judge Bernstein disagreed. Critiquing the position that implied consent can be viewed purely as a notice issue, Judge Bernstein observed that the adequacy of the disclosure statement warnings “appears to be the unspoken rationale” of the bankruptcy courts that had deemed consent by failure of a creditor to opt out. Judge Bernstein also held that a Non-Voting Creditor’s failure to return a ballot did not provide a clear indication that the creditor intended to consent to the Release. Judge Bernstein found that the small recovery under the plan or a Non-Voting Creditor’s desire not to give a release were equally plausible reasons for why some decided not to vote. [20] Accordingly, Judge Bernstein concluded that the Non-Voting Creditors did not consent to the Release. [21]

4. Bankruptcy Court Power to Enjoin Claims Without Consent

Having found that the Release proposed by SunEdison could not operate on the basis of implied consent, Judge Bernstein considered whether the Court nevertheless had the power enjoin certain third party claims under the guidelines established by the Second Circuit in In re Metromedia Fiber Network, Inc. [22] In Metromedia, the Second Circuit cited the potential for abuse in third-party bankruptcy releases, where non-debtors could shield themselves from liability and effectively discharge claims without commencing their own bankruptcy proceedings. [23] Metromedia held that a bankruptcy court has jurisdiction to approve third party releases only in “rare” and “unique” circumstances, where the releases play an important role in the reorganization. [24] Circumstances justifying a third party release may include: (1) a substantial contribution to the estate by the released parties; (2) the channeling of enjoined claims to a settlement fund rather than extinguishing them; (3) where the enjoined claims would directly impact the debtor’s reorganization by way of indemnity or contribution; or (4) where the plan otherwise provides for the full payment of the enjoined claims. [25] A non-debtor’s material contribution to the estate, without more, will not justify a third party release. [26]

In SunEdison, the Debtors argued that their indemnity obligations to various third parties (including officers, directors, and their DIP lenders) provided a sufficient nexus to justify the Release. While Judge Bernstein agreed that he may enjoin claims that would give rise to an indemnification obligation of the reorganized debtors, he noted that the Release extended far broader [27]. It enjoined any and all claims that related in any way to the Debtors or their bankruptcy cases from the beginning of time to the future Effective Date of the Plan, and covered parties like the Creditors’ Committee, estate professionals, and pre-petition senior and junior lenders to whom the Debtors did not owe an indemnity obligation. [28] For these reasons, Judge Bernstein concluded that the Debtors had failed to establish that the Court had subject matter jurisdiction to approve the Release as required by Metromedia. [29]

Judge Bernstein granted the Debtors leave to propose a modified release that would bind non-voting creditors, which (1) specified the releasees by name or readily identifiable group and the claims to be released, (2) demonstrated how the outcome of the released claims might have a conceivable effect on the Debtors’ estates, and (3) showed that this is one of the “rare cases” in which release of claims against third parties is appropriate under the Second Circuit’s Metromedia decision. [30]

5. Conclusion

Judge Bernstein’s decision in SunEdison is notable for its analysis of implied consent under New York contract law. In his view, warnings within the disclosure statement and on plan ballots were not sufficient to bind any Non-Voting Creditor to the Release, nor could such notice create a duty to speak where none existed in the parties’ ordinary course of dealing.

SunEdison should serve as a warning regarding the limits of implied consent. One noteworthy difference between the SunEdison ballots and those used by the debtors in DBSD and Indianapolis Downs was the absence of an “opt in” or “opt out” mechanism whereby creditors could make a choice to release (or not) third parties separate from the creditors’ vote to accept or reject the plan. Both the DBSD and Indianapolis Downs opinions discuss how non-voting creditors had the ability to opt out of the third party release by checking a box on their ballot, regardless of how they voted. It is unclear from Judge Bernstein’s opinion whether the inclusion of a similar provision on the SunEdison ballots would have changed his decision. At minimum, by including a separate box to opt out of a release, the plan proponent de-couples the vote for or against the plan from consent to third party releases. Whether that makes “assent by silence” easier to prove remains to be seen, but debtors who refrain from adding such provisions do so at their own risk.

A second, practical lesson from SunEdison is gained from studying the scope of the Release proposed. Without including a conspicuous opt in or opt out mechanism, the Debtors may have simply gone too far. During the plan formulation and drafting process, Debtors’ counsel was undoubtedly serenaded with a chorus of “me too” requests from creditor groups and their professionals to be included in the growing list of “Released Parties.” Ironically, in exchange for participating in the plan process, these same parties were protected by the Plan’s exculpation provisions, rendering the Release largely superfluous. As a result of this overly ambitious proposed release, the Debtors must now submit a far more limited release within the confines of Metromedia or abandon the idea of a plan release altogether. The SunEdison decision counsels discretion and moderation in drafting the release provisions in chapter 11 plans.

Notes

[1] Case No. 16-10992 (SMB) (Docket No. 4253) (Bankr. S.D.N.Y. Nov. 8, 2017) (“SunEdison”)

[2] Renewable energy projects face uncertainty during the development stage but tend to produce low-risk cash flows once they are operating. In order to attract investors to renewable energy, a parent company might transfer renewable and/or conventional long-term contracted operating assets into a dividend growth-orientated public company, known as a “yieldco.” A yieldco shields investors from development risk because assets are only transfers to the yieldco upon project completion. In the meantime, investors can expect low-risk returns (or yields) that are projected to increase over time.

[3] Eric Wesoff, SunEdison: A Timeline of the Biggest Corporate Implosion in US Solar History, https://www.greentechmedia.com/articles/read/sunedison-the-biggest-corporate-implosion-in-us-solar-history#gs.fE9oVNM (visited Nov. 9, 2017).

[4] 11 U.S.C. §§ 101 et seq.

[5] See SunEdison.

[6] Section 11.6 of the Plan provides, in full: “As of the Effective Date, subject to Article 11.8, the Releasing Parties shall be deemed to have conclusively, absolutely, unconditionally, irrevocably, and forever released, waived and discharged the Debtors, the Reorganized Debtors, their Estates, non-Debtor Affiliates, and the Released Parties from any and all Claims, Interests, obligations, rights, suits, damages, Causes of Action, remedies, and liabilities whatsoever, including any derivative Claims asserted or capable of being asserted on behalf of the Debtors, whether known or unknown, foreseen or unforeseen, existing or hereinafter arising, in law, equity, or otherwise, that such Entity would have been legally entitled to assert (whether individually or collectively), based on or in any way relating to, or in any manner arising from, in whole or in part, the Debtors, the Debtors’ restructuring, the Chapter 11 Cases, the Original DIP Facility, the Replacement DIP Facility, the purchase, sale, or rescission of the purchase or sale of any security of the Debtors or the Reorganized Debtors, including (without limitation) any tender rights provided under any applicable law, rule, or regulation, the subject matter of, or the transaction or events giving rise to, any Claim or Interest that is treated in the Plan, the restructuring of Claims and Interests prior to or in the Chapter 11 Cases, the negotiation, formulation, or preparation of the Plan, the Disclosure Statement, the Plan Supplement, the Rights Offering, the GUC/Litigation Trust Agreement, or related agreements, instruments, or other documents, upon any other act or omission, transaction, agreement, event, or other occurrence taking place on or before the Effective Date of the Plan, other than Claims or liabilities arising out of or relating to any act or omission of a Released Party that constitutes fraud, willful misconduct, or gross negligence. Notwithstanding anything to the contrary in the foregoing, the release set forth above does not release (i) any post-Effective Date obligations of any party under the Plan or any document, instrument, or agreement (including those set forth in the Plan Supplement) executed to implement the Plan or (ii) any cause of action held by a governmental entity against any non-Debtor existing as of the Effective Date based on Sections 1104-1109, 1161-1169, and 1342(d) of the Employee Retirement Income Security Act. Notwithstanding the foregoing, nothing in this Plan shall release any claims against any non-Debtor Affiliate of the Debtors arising in the ordinary course of business (i.e., ordinary course trade claims).”

[7] Section 1.194 of the Plan defined “Released Parties” to include “(a) the Debtors and all of the Debtors’ and Reorganized Debtors’ (1) current financial advisors, attorneys, accountants, investment bankers, representatives, and other professionals (collectively the ‘Debtor Professionals’); (2) current employees, consultants, Affiliates, officers and directors, including any such persons or entities retained pursuant to section 363 of the Bankruptcy Code; and (3) Existing Directors, (b) the Original DIP Agents, (c) the Original DIP Lenders and all other Original DIP Secured Parties, (d) the Replacement DIP Agents, (e) the Replacement DIP Lenders, (f) the Supporting Second Lien Parties, (g) all Professionals (to the extent not duplicative of the Entities covered by clauses (a) and (m) of this definition), (h) the Creditors’ Committee and each of its members, solely in their capacity as such, (i) the Indenture Trustees, (j) the Second Lien Collateral Trustee, (k) the Second Lien Agents, (l) any underwriters, arrangers, or placement agents in respect of the Second Lien Senior Notes, (m) the Prepetition First Lien Secured Parties, (n) the Prepetition First Lien Agents, (o) the Applicable Issuers, and (p) with respect to each of the above-named Entities described in subsections (b) through (o), such Entity’s current and former affiliates, subsidiaries, advisors, principals, partners, managers, members, employees, officers, directors, representatives, financial advisors, attorneys, accountants, investment bankers, consultants, agents, and other representatives and professionals, in each case to the extent a claim arises from actions taken or omissions by any such person in its capacity as a related person of one of the parties listed in clauses (b) through (o) and is released as against such party.”

[8] See Plan, § 1.195.

[9] See Plan, § 11.9. The Plan also included a provision exculpating various parties, including the Debtors, pre- and post-petition lenders, the creditors’ committee, and professional advisors from liability under any applicable law in connection with the Debtors’ restructuring. See Plan, § 11.7.

[10] See SunEdison at 5.

[11] See e.g., In re Metromedia Fiber Network, Inc., 416 F.3d 136, 143 (2d Cir. 2005); In re Specialty Equipment Companies, Inc., 3 F.3d 1043, 1047 (7th Cir. 1993); In re Indianapolis Downs, LLC, 486 B.R. 286, 306 (Bankr. D. Del. 2013).

[12] See In re DBSD North America, Inc., 419 B.R. 179, 218 (Bankr. S.D.N.Y. 2009).

[13] 486 B.R. 286, 305 (Bankr. D .Del. 2013).

[14] See DBSD North America, 419 B.R. at 218 (“[A]dequate notice is provided in this case, as both the Plan and Disclosure Statement have the third party release provision set off in bold font, and the ballots set forth in both capitalized and bold text the effect of consenting to the Plan or abstaining without opting out of the release.”).

[15] See SunEdison at 7.

[16] See id.

[17] See id.

[18] See id. at 10.

[19] See id. at 10–11.

[20] See id. at 11.

[21] See id. at 11.

[22] 416 F.3d 136 (2d Cir. 2005).

[23] See id. at 142.

[24] See id. at 141.

[25] See id. at 142.

[26] See id. at 143.

[27] See SunEdison at 15.

[28] See id.

[29] See id. at 16.

[30] See id. at 16-17.

This publication/newsletter is for informational purposes and does not contain or convey legal advice. The information herein should not be used or relied upon in regard to any particular facts or circumstances without first consulting a lawyer. Any views expressed herein are those of the author(s) and not necessarily those of the law firm's clients.