Cryptoasset Regulation Coming to the United Kingdom: What You Need to Know

Cryptoassets, including cryptocurrencies and other digital assets, are a global phenomenon, and they are attracting increasing regulatory attention in many jurisdictions. In keeping with this trend, the United Kingdom is finalising its regime to regulate cryptoasset businesses that are not currently within its regulatory perimeter. Those cryptoasset businesses will be brought within the UK “regulated activities regime” alongside traditional financial services businesses (such as investment banks, brokerage firms and asset managers) and distinct from the regulation of payment services and electronic money.

From 25 October 2027, in-scope cryptoasset businesses must obtain prior authorisation from the UK Financial Conduct Authority (FCA) in order to do business in the United Kingdom or provide services to certain customers in the United Kingdom. Obtaining “FCA authorisation” means those businesses will need to be licenced by the FCA, and they will be subject to regulation and supervision by the FCA in respect of their UK activities. The legislation setting out the overall framework has been finalised, but the FCA’s detailed firm-facing rules are not yet finalised. The main FCA consultation papers on these rules can be found at “Key publications” on a dedicated FCA webpage HERE.

The new UK cryptoasset regime will have a significant impact on existing cryptoasset businesses, including those that have customers in the United Kingdom, even if the business operates outside the United Kingdom and has no other UK connection or presence.

Key Takeaways

What Cryptoasset Activities Will Be Regulated?

The following cryptoasset activities will become “regulated activities” in the United Kingdom, meaning that a person carrying on such activities will generally (i.e. subject to exclusions/exemptions) need to be licensed and regulated by the FCA:

- Issuing stablecoin

- Safeguarding (i.e. custody) of cryptoassets

- Operating a cryptoasset trading platform

- Cryptoasset staking

- Dealing in cryptoassets as principal

- Dealing in cryptoassets as agent

- Arranging deals in cryptoassets

The FCA refers to the last three regulated activities collectively as “cryptoasset intermediation,” and firms undertaking one or more of these activities as “cryptoasset intermediaries.”

Note: Whilst there is no separate regulated activity in relation to advising on cryptoassets or managing cryptoassets, this does not necessarily mean that these activities are outside the UK regulatory perimeter. Instead, advising on or managing cryptoassets will be within the existing UK regulatory perimeter where the cryptoasset in question meets the definition of a type of “specified investment” in the legislation, e.g. a tokenised equity or debt security. In addition, a business that is not required to be FCA authorised may be subject to FCA requirements in certain circumstances under the “designated activities regime.”

Who Will Be Affected?

The territorial scope of the new regulated cryptoasset activities is prescribed in legislation, and this is different in some respects to the territorial scope of other regulated activities. In summary, the position is as follows:

- Firms based in the United Kingdom that undertake regulated cryptoasset activities are potentially in-scope regardless of where their customers are located.

- Non-UK overseas firms with no physical presence in the United Kingdom but providing the relevant services to consumers located in the United Kingdom are potentially in-scope. There is no specific “reverse solicitation” exemption.

Note: Overseas cryptoasset firms whose operations have UK elements will need to assess if they could fall within scope, particularly where they service consumers in the United Kingdom. There may also be some impact for traditional businesses whose activities involve cryptoassets (e.g. firms providing custody services for tokenised securities that are within scope of the new cryptoassets regime) given the different rules on territoriality for cryptoassets.

What Is the Timing?

The new regime will come into force on 25 October 2027. This means cryptoasset businesses must be authorised by the FCA by this date in order to carry on the regulated cryptoasset activities in the United Kingdom or with relevant UK customers unless the firm is able to rely on an exclusion/exemption or is within the transitional arrangements.

Note: Preparing an FCA authorisation application is a significant undertaking that for most businesses will require considerable time and resources; it will also take the FCA time to process such applications. In-scope businesses are therefore advised to start this process as soon as possible. Transitional arrangements may be available for existing cryptoasset firms that have submitted an authorisation application to the FCA before 25 October 2027 that is yet to be processed/determined. If a firm does nothing before this date, then it will have to stop operating in the United Kingdom or with relevant UK customers no later than 25 October 2027.

Consistency With the EU Regulatory Regime?

The European Union’s Markets in Crypto-Assets Regulation (MiCAR) introduced a comprehensive regulatory framework for cryptoassets in the European Union, which has been fully effective since 30 December 2024. However, the United Kingdom is not simply replicating MiCAR; the work of international bodies such as the Financial Stability Board and International Organisation of Securities Commissions has helped establish some key principles for the regulation of cryptoassets that have been adopted by both the European Union in MiCAR and the forthcoming UK regime. That said, there are differences in scope, and there are expected to be differences in the detailed regulatory requirements. It will be critically important to understand the position in each jurisdiction where a cryptoasset business operates or has customers.

Note: If your business complies with MiCAR, do not assume that what is in place will be sufficient to comply with the UK regulatory regime.

Main Aspects of the New Cryptoassets Regime

Territorial Scope

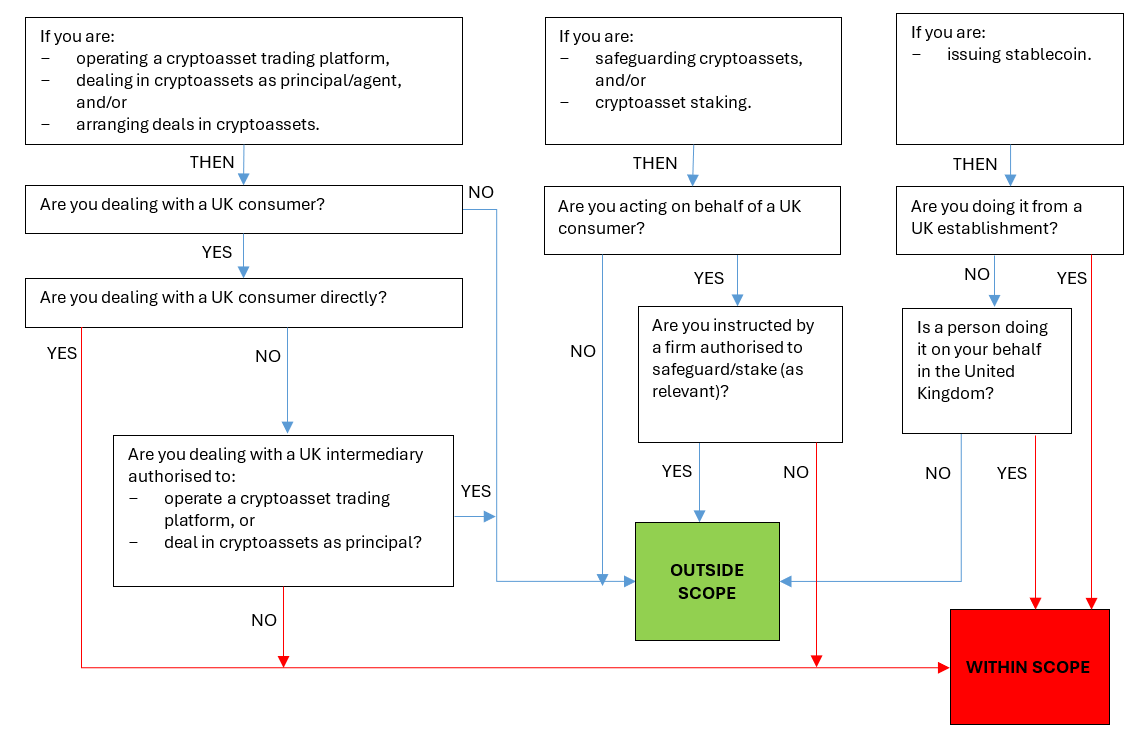

The new UK cryptoasset regime will apply to regulated cryptoasset activities carried on in the United Kingdom or provided to persons in the United Kingdom. Consequently, non-UK businesses that operate on a cross-border basis into the United Kingdom will be caught in certain circumstances even if they do not have any physical presence in the United Kingdom.

The UK Financial Services and Markets Act 2000 prescribes certain circumstances where a person is deemed to be carrying on a regulated activity in the United Kingdom even if they are not physically present in the United Kingdom. That legislation has been amended to include the following additional “deemed in the UK” circumstances for regulated cryptoasset activities:

- Where a person is involved in the sale or subscription of a cryptoasset to or by a consumer in the United Kingdom and that person is carrying on a regulated cryptoasset activity in circumstances that do not involve an FCA-authorised cryptoasset intermediary in relation to the sale or subscription.

- Where a person is carrying on the regulated activity of safeguarding cryptoassets on behalf of a consumer in the United Kingdom and is not acting at the direction of an FCA-authorised firm to carry on that regulated activity.

- Where a person is carrying on the regulated activity of cryptoassets staking on behalf of a consumer in the United Kingdom and is not acting at the direction of an FCA-authorised firm to carry on that regulated activity.

A “consumer” in this context means an individual in the United Kingdom who is acting for a purpose other than for any trade, business or profession carried on by that individual.

The chart below indicates how an overseas cryptoasset firm may be caught. Note that the chart is a simplified summary of complex requirements and is for illustration only. The specific analysis will depend on the particular facts and circumstances.

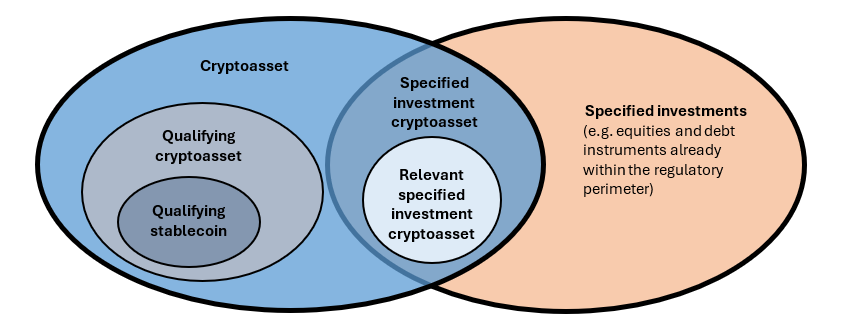

Cryptoassets That Are Within Scope

The UK regime defines a cryptoasset as “any cryptographically secured digital representation of value or contractual rights that (a) can be transferred, stored or traded electronically and (b) uses technology supporting the recording storage of data (which may include distributed ledger technology).”

Whether a particular cryptoasset is subject to the UK regulatory regime depends on whether it falls within any of the following categories:

| Regulatory Category | Definition | Relevant Regulated Activity |

| Qualifying Cryptoasset |

A cryptoasset that is fungible, transferable and not solely a record of value or contractual rights. This includes “qualifying stablecoins,” but it excludes “specified investment cryptoassets” and other instruments that are already regulated (such as electronic money). |

|

| Qualifying Stablecoin | A “qualifying cryptoasset” that seeks or purports to maintain a stable value in relation to a particular fiat currency where assets (either the referenced fiat currency or other assets) are held for the purpose of maintaining a stable value. |

|

| Specified Investment Cryptoasset |

A cryptoasset that is a “specified investment” and meets the criteria to be a “qualifying cryptoasset.” * A “specified investment” is a defined term under the UK regulated activities regime and refers to any type of investment specified in legislation that is subject to regulation (essentially financial instruments such as equity or debt security). |

See below regarding those that are “relevant specified investment cryptoassets.” |

| Relevant Specified Investment Cryptoasset | A “specified investment cryptoasset” that is within the definition of the following: “specified investments,” “security” (such as equities) or “contractually based investment” (such as derivatives). It covers tokenised versions of these instruments, such as tokenised equities. |

|

The following chart indicates the overlapping nature of the regulatory cryptoasset definitions discussed above.

FCA Authorisation

Who Needs to Be FCA Authorised?

If a firm is carrying on any of the new regulated cryptoasset activities (listed above and discussed further below) by way of business in the United Kingdom or with relevant UK customers, and no exclusion/exemption is available, the firm must obtain prior authorisation from the FCA for the specific activities it wishes to carry on, whether or not they are already authorised by or registered with the FCA for other activities. Being FCA authorised means the firm will be licensed and subject to regulation and supervision by the FCA.

This is expected to impact existing businesses as follows:

- For existing cryptoasset firms that are currently required to be registered with the FCA under the UK anti-money laundering (AML) requirements, they will need to consider whether they are within the scope of the new regime and accordingly whether they need to apply to be authorised and regulated by the FCA.

- For existing FCA-authorised traditional financial services (e.g. investment firms), they will need to consider whether they are brought within scope of the new regime. This might be the case if, for example: (i) they are carrying on or begin to carry on one or more of the regulated cryptoasset activities, or (ii) they undertake safeguarding (custody) activities for tokenised traditional asset classes.

Businesses based outside the United Kingdom that need to be authorised by the FCA will need to establish a UK presence. That might involve establishing a UK subsidiary or a UK branch (for overseas cryptoasset platforms that fall within scope, that might involve establishing both a UK subsidiary and a UK branch). The FCA is consulting on these options.

Carrying on a regulated activity in the United Kingdom without the requisite authorisation is a criminal offence which may result in imprisonment and/or unlimited fines. In addition, certain of the exemptions from the new prohibition on public offers of cryptoassets in the United Kingdom are dependent on the involvement of an appropriately FCA-authorised cryptoasset firm (discussed further below).

What Do the Regulated Cryptoasset Activities Entail?

Further details of the new regulated cryptoasset activities and associated requirements are set out below. Note that there are exclusions/exemptions from the regulated activities (not discussed in this article) which may be available depending on the facts and circumstances.

| Issuing Stablecoin |

The regulatory meaning of “issuing” does not necessarily track the concept currently understood in the market. For firms involved in the stablecoin redemption process, careful analysis would be needed to avoid being inadvertently regarded as “issuing” the stablecoin. Firms that deal with qualifying stablecoin but that are not “issuing” may need to consider if they could be within other regulated cryptoasset activities (e.g. one of the cryptoasset intermediation activities). |

| Safeguarding of Cryptoassets |

This activity extends to “relevant specified investment cryptoassets” (discussed above). Relevant specified investment cryptoassets, such as tokenised shares, are expressly carved out of the current regulated activity of safeguarding and administration of assets. This means custodians currently providing custody services for tokenised instruments on the basis of their existing FCA permission for safeguarding and administration of assets will need to consider whether they have to vary their FCA permissions to add this new regulated cryptoasset activity or whether an exemption is available. |

| Operating a Cryptoasset Trading Platform |

|

| Cryptoasset Staking |

|

| Cryptoasset Intermediation Activities (i.e. dealing in cryptoassets as principal or as agent, and arranging deals in cryptoassets) |

|

What Requirements Must Be Complied With Once Authorised?

An FCA-authorised cryptoasset firm must comply with various requirements, including maintaining financial and nonfinancial resources, as well as conduct of business requirements. We set out below some of the main requirements as currently understood. As mentioned, the FCA is still to finalise the rules.

| Regulatory Capital Requirements |

This is the amount of cash (and other permitted assets) that must be maintained at all times. This must be the highest of the following three components:

|

| Overall Risk Assesment Requirements |

|

These requirements include:

All authorised cryptoasset firms must review their overall risk assessment at least annually or immediately following any material change. |

| Liquidity Requirements |

|

These set out the form and amount of liquid assets that must be held.

This must be in the form of on-demand deposits at a UK bank. |

| Disclosure Requirements |

Authorised cryptoasset firms must publicly (e.g. on their websites) disclose required information, including information on:

|

| Other Applicable Requirements |

|

Requirements under the FCA Handbook (which contains detailed rules for FCA-authorised firms)

Other aspects of financial services laws and regulations

|

Additional Requirements Relevant to Cryptoasset Businesses: Designated Activities Regime

The United Kingdom’s recently introduced “designated activities regime” empowers the FCA to impose requirements on firms that are not authorised by the FCA if they are carrying on a “designated activity” in the United Kingdom. This regime is being used to impose the following requirements in relation to cryptoassets:

| Cryptoasset Public Offers and Admissions to Trading |

|

| Market Abuse in Cryptoassets |

|

Transitional Arrangements

There are two transitional arrangements for existing cryptoasset firms that would come within the new regime. These are called the “saving provisions” and the “transitional provisions.” In summary:

Saving Provisions

If the firm applies for authorisation within the period from 30 September 2026 to 28 February 2027 (application period) and, by 25 October 2027 (the go-live date), the application is still open (e.g. the FCA has not decided whether to grant authorisation), then the firm enters into the “saving provisions.” This means that the firm may continue operating its business as usual until the application is determined.

Transitional Provisions

If the firm applies for authorisation and the application has been refused within the above application period, or if the firm applies for authorisation after the application period but before 25 October 2027 (the go-live date) and the application is still open by 25 October 2027, then the firm enters into the “transitional provisions.” This means that the firm may only operate its business in relation to pre-existing contracts (e.g. contracts entered into before the FCA refusal) and it may not take on new customers.

There is a long stop date for both arrangements, which is 25 October 2029. If a firm applies for authorisation after 25 October 2027, it must stop the UK business while waiting for the outcome of the application.

Not to Be Forgotten

Certain aspects of current UK law applicable to cryptoasset businesses will continue to be relevant under the new cryptoasset regulatory regime, but with some changes. We note in particular the following:

| Current | Future Under New Regime | |

| AML Registration |

Certain cryptoasset businesses–“cryptoasset exchange providers” (CEP) and “custodian wallet providers” (CWP) – must register with the FCA for AML purposes. (CEPs provide exchange services between fiat and cryptoasset or between different cryptoassets; CWPs provide custody of others’ cryptoassets.) Note: This registration is not a regulatory licence or authorisation. |

The AML registration regime remains. Cryptoasset businesses that are not required to be authorised by the FCA under the new cryptoasset regime (e.g. due to an exemption) may still need to seek AML registration and comply with that regime. |

| Cryptoasset Financial Promotion |

Cryptoasset promotions (e.g. marketing) are prohibited unless exemptions are available. This applies to promotions relating to the following cryptoasset activities:

|

The cryptoasset promotion restriction will be expanded to cover the following new cryptoasset activities:

|

| Ban on Selling and Marketing Cryptoasset Derivatives | Certain UK-authorised investment firms (such as securities dealers/brokers) are banned from selling or marketing cryptoasset derivatives to retail investors in the United Kingdom. |

The FCA proposes to not apply these bans to authorised cryptoasset firms under the new regime. However, given that the FCA generally considers cryptoasset derivatives to be securities, authorised cryptoasset firms may not be able to deal with them unless they also have the relevant FCA permissions relating to such securities. |

How Might the Regulated Activities Regime Apply to Different Cryptoassets?

The FCA previously issued guidance on cryptoassets (PS19/22) in July 2019, which described different types of cryptoassets and the expected application of the existing UK regulatory regime at that time (i.e. 2019) to them. We set out below some thoughts on how the UK regulatory regimes might apply to the different types of cryptoassets identified by the FCA in light of the forthcoming UK cryptoasset regime.

| Types of Cryptoasset | Description/Usage | How Might the UK Regimes Apply? |

| Exchange Token | Usually decentralised and primarily used as a means of exchange. Sometimes known as “cryptocurrencies,” “crypto-coins” or “payment tokens.” Designed to provide limited or no rights for token-holders, and there is usually not a single issuer to enforce rights against. |

These tokens may be within the existing regulated activities regime or the new cryptoasset regime, depending on whether a given token could be characterised as qualifying cryptoasset or specified investment cryptoasset. A given token may also trigger other regulatory regimes, such as AML registration discussed above or payment services/e-money regulation (not discussed in this article). The analysis will turn on the token’s substance rather than how it is labelled, as well as how the token is used. |

| Security Token | Tokens that provide rights and obligations akin to the types of investments that are already regulated (e.g. shares, debentures and units in collective investment schemes), including tokenised versions of those traditional asset types. |

The FCA indicates that they would regard such security tokens as “specified investment cryptoassets” under the new cryptoasset regime. Consider if the security that is tokenised is or has the characteristics of a specified investment, and if so whether it is a “relevant specified investment cryptoasset.” |

| Utility Token | Tokens that provide consumers with access to a current or prospective product or service and often grant rights similar to pre-payment vouchers. |

These tokens may be within the existing regulated activities regime or the new cryptoasset regime, depending on whether a given token could be characterised as qualifying cryptoasset or specified investment cryptoasset. A given token may also trigger other regulatory regimes, such as AML registration discussed above or payment services/e-money regulation (not discussed in this article). The analysis will turn on the token’s substance rather than how it is labelled, as well as how the token is used. |

| Non-Fungible Token (NFT) | Confer digital ownership rights of a unique asset (e.g., a piece of digital art). |

Generally not expected to be within the existing regulated activities regime or the new cryptoasset regime. A given NFT may trigger other regulatory regimes, such as AML registration discussed above or payment services/e-money regulation (not discussed in this article). The analysis will turn on the NFT’s substance rather than how it is labelled, as well as how the NFT is used. |

This publication/newsletter is for informational purposes and does not contain or convey legal advice. The information herein should not be used or relied upon in regard to any particular facts or circumstances without first consulting a lawyer. Any views expressed herein are those of the author(s) and not necessarily those of the law firm's clients.